The first indication that Barloworld – a cornerstone of SA’s industrial sector for more than a century – was in play came on April 15 this year.

But the cursory cautionary warning shareholders that Barloworld had entered into discussions “which may have a material effect” on its share price gave no clue that CEO Dominic Sewela was a key player in the talks as a potential buyer, and not as the steward managing it through such a scenario on behalf of shareholders.

Or that, in fact, Sewela had first approached the Barloworld board as early as February with the idea.

The same detail-free cautionary was renewed again four times before, on October 15, Barloworld confirmed there was a takeover offer. Still, investors had to wait until November to learn the identity of those behind the R22.8bn bid: a consortium including Sewela’s newly formed company, Entsha.

On the face of it, the offer isn’t to be sneezed at: Sewela’s group is offering R120 a share – an 87% premium to the R65.72 average price at which Barloworld’s shares traded in the month before the first cautionary came out.

But for Aeon Investment Management portfolio manager Asief Mohamed, it is Sewela’s position on both sides of the fence that is an ominous red flag.

“The CEO of Barloworld should have disclosed his interest in the acquiring consortium much earlier and recused himself from all related discussions,” he tells Currency. Mohamed tried to talk to Sewela about this conflict of interest, but he says Sewela wasn’t interested.

The failure to publicly disclose the CEO’s involvement in takeover talks – where he is in a position to play both sides in a high-stakes gambit – is compounded by what some analysts fear may be a supine board, which should have appointed a caretaker CEO the minute Sewela showed his hand.

“This is not an independent board – they are doing what he wants here,” says one veteran corporate financier.

Mohamed agrees. “The board should have insisted the CEO step aside, appointing an interim, unconflicted CEO. The significant delay in announcing the transaction details exacerbated the CEO’s untenable conflict of interest,” he says.

While local rules do allow for a CEO’s involvement in a buyout of the company he or she runs, the corporate financier, who asked not to be named, says: “It’s very difficult to do something like this that is not going to prejudice the company.”

He says it is “crazy” to have a CEO still running the company while the deal is finalised, which could take a year. “If I was on that board I’d definitely park him on the bench and get someone else to caretake the business. Every day there are going to be trade-offs and there’s no-one there managing it.”

‘Governance protocols’

In response to questions from Currency, Barloworld’s board spokesperson Michelle Strauss says there is a “clear delineation” between the day-to-day operations of the company, and anything related to this deal. “The board is confident that sufficient safeguards are in place to ensure that the company is managed efficiently and with minimal disruption,” she says.

Asked why the board has not appointed an acting CEO while this deal is negotiated, Strauss says: “Management buy-outs are not uncommon in public markets. From the time of the initial approach, the CEO was, and continues to be, recused from all Barloworld-related issues on the proposed transaction.”

A steering committee of non-conflicted executives and external advisers has been created, which has been “tasked with assisting the independent board” to assess the deal, she adds.

But how this sort of wall is erected in practice, and whether it can really be effective, remains in doubt.

After all, the “independent board” constituted in February to handle the bid consists of members of its current board: chair Lulu Gwagwa, lead independent director Neo Mokhesi, Peter Schmid, Nicola Chiaranda and Vuyisa Nkonyeni.

This board, said Barloworld last week, “introduced clear and enhanced governance protocols to address any concerns that may result from the CEO’s involvement in the consortium and the proposed transaction”.

The “governance protocols” are as woolly as you might expect. Besides “non-disclosure agreements” with consortium members (including the CEO and members of the Barloworld executive committee), these include Sewela himself “minimising” potential conflicts of interest between his duties as a director, employee and his personal interests.

It goes on: the CEO agreed to “minimise disruption to the operation of the company” and not share “any confidential information with the consortium without the independent board’s consent”.

One of the concerns is that Barloworld’s board is still relatively new, with many directors only joining in the past 10 years, many after Sewela’s own appointment in February 2017. Gwagwa, for instance, only took over three years ago, after lawyer Dumisa Ntsebeza retired in 2020 following a 13-year stint as chair.

The last thing any Barloworld shareholder would want at this point is a weak or inexperienced board, unable to stand up to a CEO trying to buy the company.

One portfolio manager, who asked not to be named, says his firm sold out of Barloworld specifically over “governance and other related” concerns.

Resistance builds

Tellingly, some shareholders have already voiced their opposition to this deal.

Silchester – a shareholder which speaks for 17.7% of Barloworld’s stock – has drawn a line in the sand, saying it will not sell for less than R130 a share, implying Sewela’s consortium would have to hike its offer nearly 10%.

The UK-based investment firm says that while the past few years have “been challenging for Barloworld”, it believes that with “new management, a reasonable board of directors, and proper capital allocation”, the company would be “well-placed to succeed in the coming years”.

This sets the stage for a stand-off, not least because Silchester warns that any takeover of Barloworld is unlikely to succeed “without the support of Barloworld’s primary shareholders”, itself included.

Certainly, you would expect any buyer to have to pay top dollar to snaffle an aristocrat of South African industry.

While Barloworld has had a stop-start trajectory over the past decade, it was once one of South Africa’s pre-eminent industrial powerhouses.

Founded by Major Ernest Barlow in 1902, the company started out selling wool products and engineering equipment. Its big break came in 1927 when Charles “Punch” Barlow, Ernest’s son, secured the rights to distribute Caterpillar products in South Africa.

From then on, Barlows was the face of South African industry – from mining to motor cars, and just about everything in between during the closed decades in which South African firms became bloated conglomerates thanks to apartheid restrictions on expansion abroad.

Since Sewela took over in 2017, Barloworld has been on something of a roller coaster ride, however.

The first major decision he took was to sell the company’s Spanish and Portuguese Caterpillar franchises to Italian company Tesa for $180m.

Barlow’s veterans were astounded. Caterpillar franchises are as rare as hens’ teeth and often passed down from one generation to another, one industry veteran says. The idea was to cut debt, but two years later Barloworld bought Tongaat Hulett’s starch business for almost double what it got for selling the Caterpillar franchise.

This Tongaat deal was surprising, not least because Barloworld is often criticised for being too much of a patchwork of different businesses. Yet all of a sudden, says one former staffer, apparently it made sense to “have a starch business and a construction business in the same stable”.

In 2022, Barloworld then sold its logistics and motor retail business, and listed its car rental unit, Zeda, which includes the Avis and Budget brands, on the JSE.

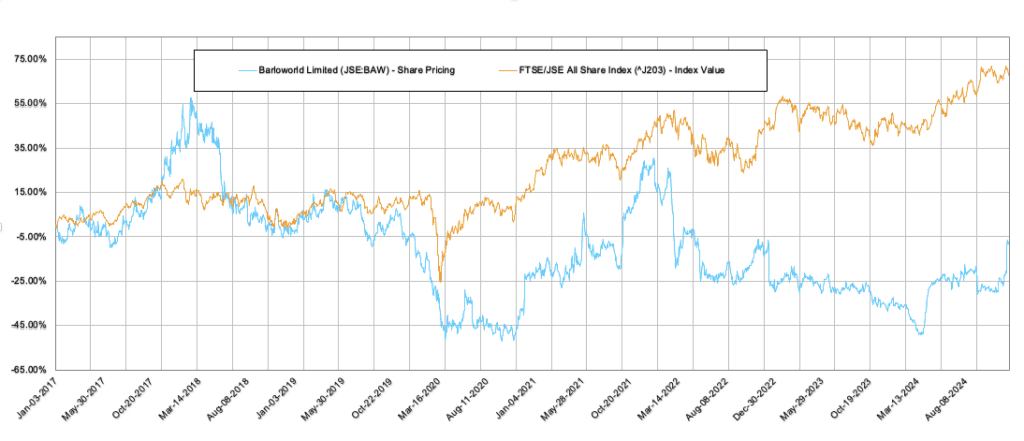

The result has been a share price which has lagged the JSE all share by an unsettling 75% during Sewela’s stewardship — and that is even after the healthy 20% bump over the past month provided by the takeover offer.

The Russian curveball

So what does this proposed takeover look like?

The buyers’ consortium includes Entsha – a company created by Sewela’s family trust – and Gulf Falcon, a subsidiary of the Riyadh-based Zahid Tractor & Heavy Machinery.

Besides haggling over the price, there are a couple of sizeable risks to the deal going through. One such risk is the potential “export control violations” related to sales of certain goods to Barloworld’s Russian subsidiary.

Back in September, the company warned that it had submitted an “initial notification of voluntary self-disclosure” to the US department of commerce and the Bureau of Industry and Security (BIS) regarding these “violations”.

“The precise details of whether there had been violations and if so, the extent of such violations, have not yet been determined, and remain subject to the above-mentioned investigation and voluntary engagements with BIS,” it said.

There is little detail about what went down, but Barloworld is one of the few companies that hung on to its Russian assets after Russia’s invasion of Ukraine, as it was the official Caterpillar dealer for the region.

You can see why: the Russian business brought in R4.24bn in the year to end-September – roughly 10% of Barloworld’s total R41bn turnover, though that was down from R5.34bn the year before. According to Daily Maverick, the Russian business accounted for 23% of turnover before the war began.

The sticking point is that these “export violations”, as well as sanctions, have been flagged by the bidders as possible “material adverse changes”. In other words, if there is a big fallout because of this, Sewela’s consortium can walk away.

Richard Cheesman, founder of Urquhart Partners, tells Currency that between the low-ball offer price and the “get out of jail free card” if anything comes from the export violations, “there is a reasonable chance that the transaction does not go through.”

Cheesman says that based on the rise in Barloworld’s stock, the odds implied by the market suggest there is a two-thirds chance that the deal does happen.

“If the deal fails, the share price will decline a bit. It’s not too expensive (normalised earnings per share are probably more than R10), and being potentially still considered in play, it may not fall that much,” he says.

Quite what will become of Zahid if the deal fails is another question entirely.

The Saudi group began buying up Barloworld shares in 2020, and now owns 18.9%, making it the second-largest shareholder after the Public Investment Corporation, which owns 20.8%.

“It seems unlikely they would walk after only trying once,” reckons Cheesman.

He’s less fazed by Sewela’s involvement in the consortium, but reckons a big question is how Newco is funding the transaction.

“Is Zahid fully financing Newco, and if so on what terms? Depending on the terms of any financing arrangement, potentially most of the economics may yet accrue to Zahid. The circular might reveal more to these ends, we will have to see,” he says.

This illustrates how high the stakes are – not just for the face of South African industry, but for Sewela himself.

If the deal fails, says one analyst, “then you’re in a funny place where this board needs to change and the CEO needs to be kicked out”.

Either way, you can be sure that a year from now, the fate of the industrial vanguard which began life as Barlows back in 1902 will look entirely different.

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.