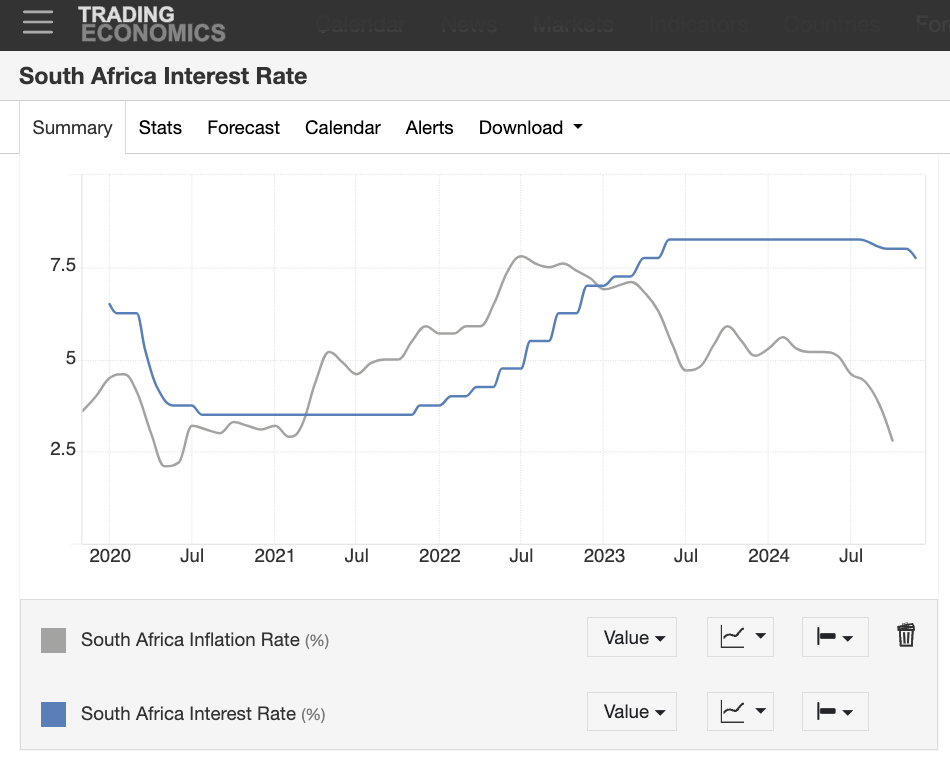

The South African Reserve Bank’s monetary policy committee (MPC) cut interest rates by 25 basis points (bp) yesterday, inviting an unusual question: what is the actual point of setting a target if you can’t muster the courage to alter course when inflation drops below it?

The MPC was on course to drop interest rates by a quarter of a point even before South Africa’s inflation rate of 2.8% was announced on Wednesday, slightly below expectations. It held to that course on Thursday, despite the fact that the inflation rate is now below its 3% to 6% target range.

The MPC justified its caution on the basis that though inflation was lower, risks were higher.

Reserve bank governor Lesetja Kganyago said a 50bp drop did not even feature in the MPC’s discussion, and the 25bp call was unanimous.

Kganyago classified “material upside risks” to be something he described as a “more difficult external environment”, which could result in a weaker rand and higher oil prices.

Behind this explicit notion of a more difficult external environment, there was a very obvious unspoken one: the election of Donald Trump as US president.

Kganyago was asked specifically about how Trump’s election might have changed the local inflation outlook, and he demurred, saying reserve bank governors don’t comment about heads of state, especially foreign ones.

But in a sense, the fact that the committee was so palpably determined to hold its course and not accelerate its interest rate reduction programme was comment enough.

Trump’s support for higher US tariffs and his reputation for being generally unconcerned about the level of US national debt has changed the inflation outlook internationally, illustrated most immediately by the rising dollar.

“The disinflation process is there, but it is clearly a very bumpy road and it is making central banks cautious across the globe. As a central bank in a small open economy, caution is what is going to be at play,” Kganyago said.

‘Missing the bigger picture’

The MPC decision was generally anticipated by the market, and all 20 economists surveyed by Bloomberg expected the decline to 7.75% from 8%. Yet it was not unanimously welcomed.

Fund manager at Sterling Private Wealth Joanne Baynham tweeted before the decision: “Monetary policy is far too restrictive in SA. The cost of capital is far too high – businesses hire people. It’s not rocket science. We need rate cuts and 25bp won’t cut it.”

Baynham said in an interview that though she supported the Reserve Bank’s cautious approach, “there is a difference between caution and extreme caution”.

Ultimately what drives inflation is a decrease in competition, but in South Africa, because the cost of capital is so high, businesses are unable to get off the ground to create that competitive increase, she said. “I think they [the Reserve Bank] sometimes miss the bigger picture”.

The Reserve Bank has essentially put interest rates up 10 times between 2021 and 2022 while inflation increased from 3% to 8%. But it has decreased interest rates only twice, and each time only by 25bp, while inflation has entirely reversed that rise.

Inflation is now below the bottom of the targeted rate, opening a debate about what actually is the bank’s true target, particularly after Kganyago has openly suggested that a 3% target would be appropriate, and is currently in discussion with the Treasury on that topic.

But he denied the bank was implicitly or informally targeting 3% at the moment. “So if you set a target and it’s secret … but you are targeting it quietly, it’s not useful as a policy anchor. We have a process with the Treasury that we believe is coming to a conclusion. I can’t quite give you the timeline because the debates have become very, uh, rigorous.”

The committee’s caution was also expressed in its decision to increase its inflation projection over the medium term. “It will gradually go up towards the midpoint of our target. It will remain below the target until mid next year, and then start moving upwards.” But the suggested increase in the bank’s inflation expectations is small, suggesting it’s not anticipated huge changes in the global or local outlook.

The next MPC meeting is in January.

Top image: Reserve Bank governor Lesetja Kganyago. Photo by Gallo Images/Frennie Shivambu

Sign up to Currency’s weekly newsletters to receive your own bulletin of weekday news and weekend treats. Register here.